-

Call options demystified using Jeff Bezos’s super-mega yacht

Options are often difficult to understand, but read this article, and I can almost guarantee you’ll be a lot more knowledgeable about how they work.

We’ll begin with a boring practical real-world example followed by a silly analogy which will burn it into your memory permanently!

What is a call option?

A call option is a contract that you enter with the option seller. Buying a call option gives you the right to buy a stock, say, Shopify (SHOP), for a price you choose (the strike price) within a certain number of days.

Remember: all options expire after a certain number of days. Options with expiration dates that are further away are more expensive because of the time value of money and the increased risk to the option seller that the stock price will go up and hit the strike price.

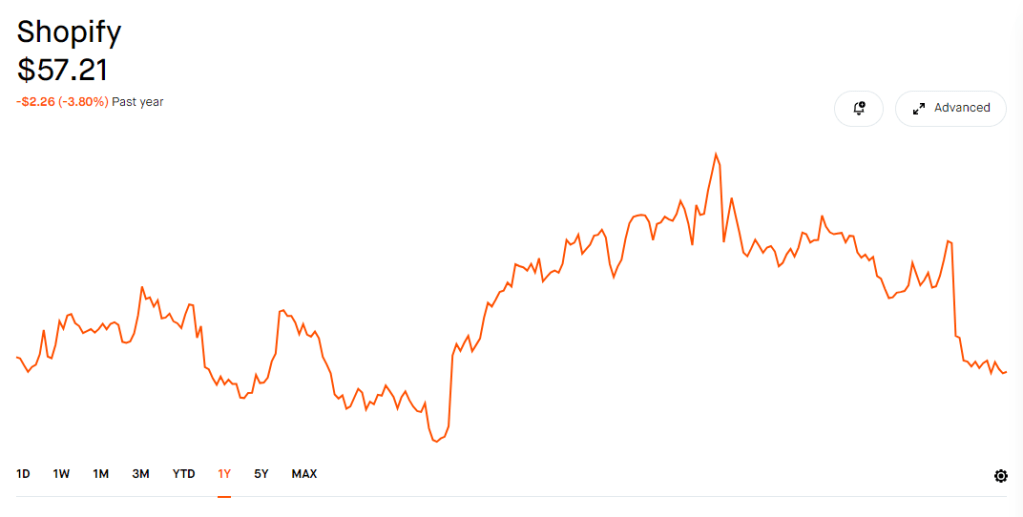

Let’s say you think Shopify has bottomed out and you want the right to buy 100 shares of the stock for the next 30 days.

As you can see by the chart, it dipped quite a bit post-earnings, but appears to be hitting some resistance!

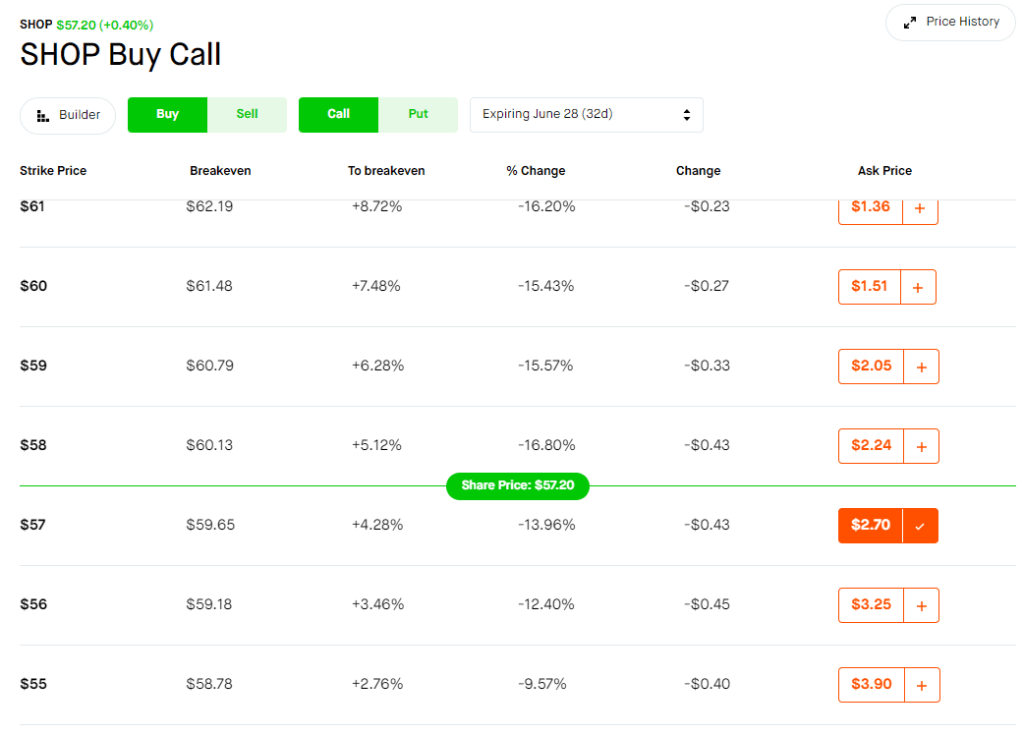

So, you go to the option chain and buy a call option with the following parameters:

- Strike price: $57

- Price paid to enter the option contract (Premium): $270 (or, $2.70 per share)

- Expiry date: June 28 (32 days from now)

The stock is currently trading at $57.20, but you need it to increase a bit more so that it becomes worth it to exercise your option. You need the stock to surpass your “breakeven point.”

Your break even price is calculated as follows:

$57.00 + $2.70 = $59.70

That means, if Shopify’s stock price rises above $59.70 per share, it would become worth it to exercise the option for your right to buy 100 shares at $57/share.

For example, if the price rose to $65, and you exercised your option, your all-in cost per share would be the $57 per share you paid to buy the stock, plus the $270 you paid to enter the option contract.’

Your total cost would be calculated as follows:

$5700 + $270 = $5,970

Or: $59.70 break-even price x 100 shares = $5,970

You could the turn around and sell the shares for the prevailing market rate of $65 per share and make a profit.

Your profit would be calculated as follows:

$6500 (100 shares at $65 per share) – $5,970 (your all in cost) = $530 (your profit)

Remember, if the stock doesn’t rise above the break-even price, the $270 call option you bought expires worthless.

Understanding call options through a silly analogy

Pretend you’re a bazillionnaire.

After a night of heavy drinking, you decide you want to buy Jeff Bezos’s super-mega yacht. Unfortunately, Jeff has another potential buyer: Dua Lipa.

How Jeff looks at you when you offer to buy his super-mega yacht Before you buy it, you want to check with your accountant to make sure buying a super-mega yacht is a good investment. In order to buy yourself some time to do this, you offer to pay Jeff $50,000 today in exchange for the right to buy the super-mega yacht within the next 14 days for the low-low price of $100,000,000.

The next day, you wake up feeling sober enough to talk to your accountant, who persuades you that buying a super-mega yacht is not a fiscally prudent move. You grudgingly agree.

After 14 days of ignoring Jeff, who had since been blowing up your phone (no doubt inquiring over your interest in buying the yacht), you allow the option to buy the yacht to expire.

This means that Jeff’s obligation to keep the super-mega yacht available for you in case you wanted it has lapsed and he is now free to turn around to sell it to Dua Lipa or to whoever else wants it.

Unfortunately, this means he gets to keep the $50,000 you gave him for the option to buy it, since the time constraint in the contract has been met. Using option-trader lingo: the option you bought expired worthless.

Fortunately for you, you’re better off wasting $50,000 than $100,000,000 on a super-mega yacht. Perhaps the rubber dingy collecting dust in your garage is really all you needed to have a good time after all. Besides, you know what they say about the word boat: it stands for “Bust out another thou!”

Awesome story, but what does it have to do with options?

The data points in the above example are analogous to the three main components of an option:

- $50,000: is analogous to the option premium you pay to buy a call option

- $100,000,000: is analogous to the strike price – the price you lock in and at which you can buy 100 shares of the underlying stock

- 14 days: is analogous to the expiry date of the option. Remember: all options expire!

If you can understand this example, you’ve got the concept down.

-

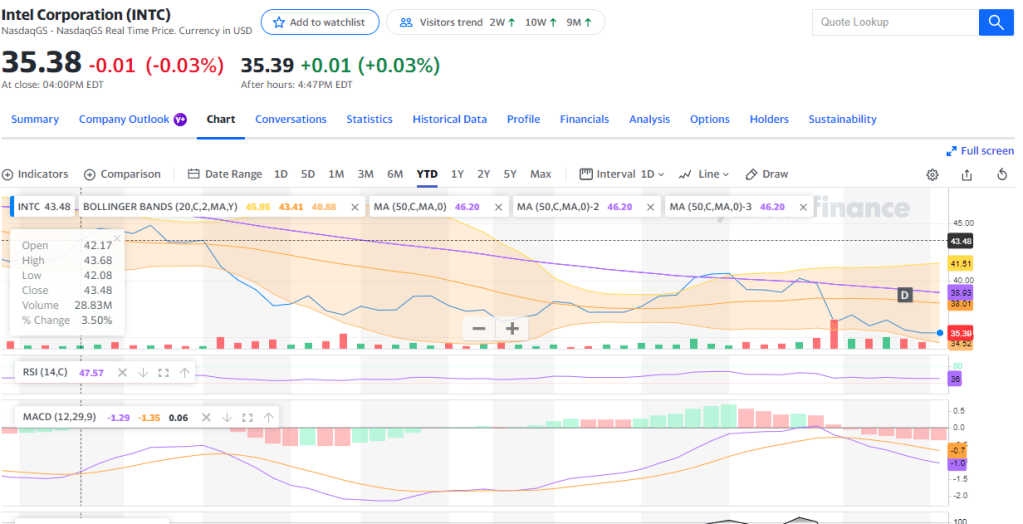

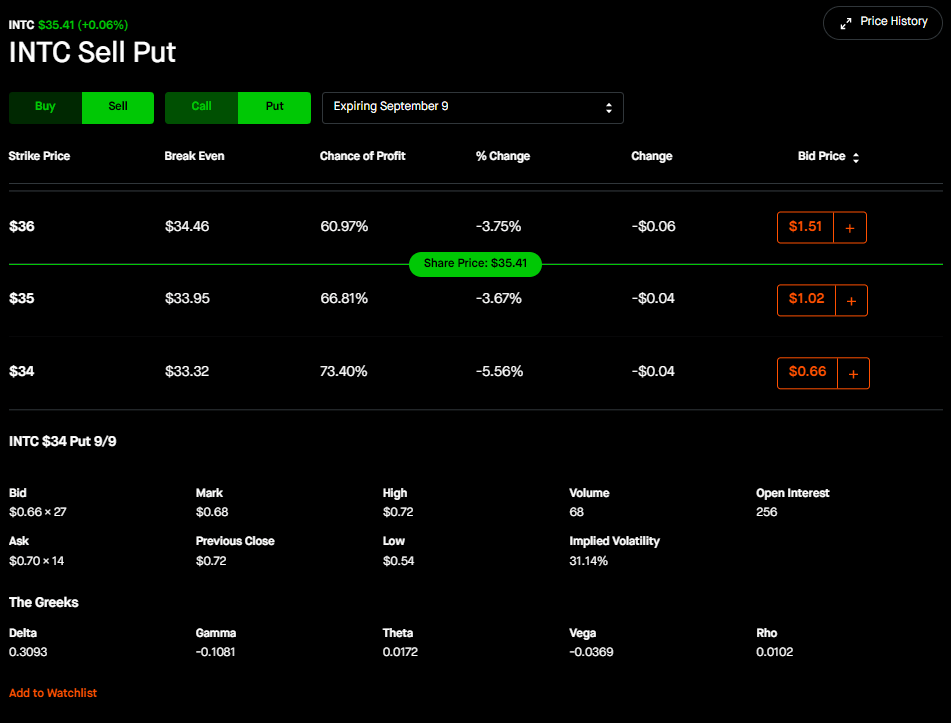

Has Intel (INTC) bottomed?

Intel has been hovering near it’s 52-week low. With an attractive 4% dividend yield and trading at just 7.6 times earnings, you may be asking yourself if it’s time to take the plunge.

Its current price needs to be looked at in the context of its fundamentals, long-term prospects and its arms-race with Nvidia and AMD. The question of which of these companies will dominate the industry is outside the scope of this article, but suffice to say, Intel is trading at about 1.4 times its book value and despite its dwindling revenues, it continues to be the dominant player in the American semiconductor space.

That throat-clearing aside, the fundamentals seem attractive. In addition to being near its 52-week low, Intel is also trading near the bottom of its Bollinger Band.

The option play

With an implied volatility in the low 30s, Intel’s options may not be the most lucrative, but they’re certainly worth taking a look at. Given its proximity to its 52-week low and it’s history of dividend rate hikes, selling puts a month out might be a fairly low-risk play.

With its disappointing earnings report now firmly in the past, I like the $34 strike with a delta of about .31. This translates to an annualized return of about 23%.

Alternatively, if you wouldn’t mind owning the stock, you can risk selling a put that’s closer to the money. A strike of $35 will yield an annualized return of about 31%. If you get exercised, you can immediately turn around and sell near-the-money covered calls to generate some lucrative premium income. The likelihood of Intel’s price sinking too far is low given its place in the Bollinger Band and the fact that the market has probably digested the worst conclusions of its last earnings report by now. The additional up-front income from the covered calls would significantly reduce your cost basis, which is why I’d recommend selling a near-the-money call option if you do decide to go with the $35 strike.

The put option premium you generate from either the $34 or $35 strikes in conjunction with the premium you collect selling near-the-money calls and that juicy 4% dividend would meaningfully reduce your cost basis and help cover your downside risk if your puts get exercised.

Where to trade options

I use Robinhood to trade options. I have other brokerages for my more passive portfolios and my 401(k), but I do not trade options on any of them.

I recommend Robinhood because of its easy to understand GUI and low fee structure.

Sign up here and get a cash bonus along with a free share of stock!

-

Robinhood: the people’s champ

Robinhood has gotten a bad rap over the years – much of it undeserved. In the medieval 90s, the only way trading stocks would be worth your time is if you had a significant amount of money and planned on buying and holding for a long period of time. Trading fees were high, which meant that if you had a small portfolio, your profits would probably be wiped out by the fees you would pay to enter and exit a position. This was the norm for many years until Robinhood disrupted the industry, forcing the legacy brokerages to follow suit.

Photo by Andrew Neel on Pexels.com Robinhood was not only the pioneer when it came to eliminating trading fees, but they are also the reason you can buy a fractional share of stock. These are the two elements that really democratized investing for the masses. If that weren’t enough, they also introduced option trading to millions of people globally, opening up an avenue for wealth-building that was, until they entered the scene, only available to the relatively affluent.

As if all that weren’t enough, the user-friendliness of Robinhood’s GUI and the appealing design are just icing on the cake. It must be said plainly: despite its critics, Robinhood is simply in a league of its own, and no other brokerage comes close or even tries to.

Of course, like any company, they have their issues. The main complaint I hear from people is that their customer service isn’t the best, which may be true, but they’re hardly alone on that charge.

I use Robinhood for my option-trading and have no intention of moving to another brokerage any time soon. I do have other brokerages for my more passive portfolios and my 401(k), but Robinhood is currently the only brokerage I use to trade options.

If your interest is piqued, you can sign up using this link and get a cash bonus along with a free stock.

Happy Trading!

-

Time to buy oil MLPs

Photo by Suzy Hazelwood on Pexels.com For a relatively safe value play, MLPs and midstream companies offer low volatility and attractive dividends. Warren Buffet has recently increased Berkshire’s stake in Occidental Petroleum, so if you’re feeling like you’ve missed the boom in oil & gas, you’re in luck.

While oil exploration companies are trading near all time highs, midstream companies are still at relatively decent valuations. In addition, they offer attractive dividends yields. Two stocks I have alternately sold puts on or owned outright with good results are Energy Transfer (ET) and Enterprise Products (EPD), both of which have current dividend yields of about 7%.

In fact, any time either of these two companies hit a floor, I dive back in and wait for the inevitable bounce in price. (Usually using a near-the-money put option.)

The options play

EPD and ET are solid value stocks, and as such, have low implied volatility. That is to say, the option premium you collect won’t be as high as a stock with an implied volatility of say, 40%. (EPD’s implied volatility is about 27%.)

So while EPD and ET are not exactly ideal targets for selling options like puts or covered calls, you can still use these strategies to easily crank out a return somewhere in the mid-teens. (I was able to generate an annualized ROI of 15% by holding EPD and selling covered calls.)

In the current environment, and with rising inflation, owning a solid value stock that pays a healthy dividend may not provide the best returns, but in the worst case, is a safe place to park some capital and generate cash while waiting for more lucrative plays. EPD is financially healthy, currently trading at a little over twice its book value – not a bad valuation considering its attractive dividend yield.

Besides, who can turn up their nose at a 15% return?

-

How to stop losing your shirt trading options and the rise of “Loss Porn” on WallStreetBets

Photo by Anete Lusina on Pexels.com While it can be therapeutic to realize other people have lost more money than you have (so much more), it’s also beneficial to remind yourself that the objective of investing is not accumulate war stories to share with strangers on the internet.

If you’ve consistently lost your shirt, there’s no need to resign yourself to what WallStreetBets politely refers to as a future trading sexual favors behind the Wendy’s dumpster. So let’s rip off the Band-Aid and be real for a minute. If you are consistently losing money, you need to stop doing these things.

Buying leap options on hyped up growth companies

All this does is guarantee you lose your collateral a year or two from now. If the little voice in your head starts telling you about the time value of money and how the loss won’t be so bad because you can take it as a tax deduction, you’re probably already in pretty deep and need to consider taking a small or medium sized loss before it turns into a big loss.

It’s best to close these positions out and try to either net them to zero or eat a loss if you have to. Remember, a 50% loss is better than a 100% loss. It can be hard to know when to take a loss on a trade, but it gets easier with experience.

I am not saying you shouldn’t have a few risky growth stocks in your portfolio – I do too – but you cannot afford to have nothing but risky growth stocks with great PR and no revenue in your portfolio!

Having spreads be the majority of your option positions

Selling spreads is alluring because of the relatively low collateral required to make great returns. However, it’s a fairly risky play and one bad spread can wipe out your profits from 10 good spreads. You really really need to know what you’re doing before dabbling in spreads. I actually don’t even consider them to be a proper investments, but rather, more in the arena of raw speculation. This is because if you sell a call credit spread, and the underlying security blows through your strikes, you’ve basically lost your collateral. It may only be $100 or $500 or $1,000, but this can decimate a small account, and fast.

Instead of selling spreads, especially starting out, stick with puts. The returns won’t be as high, but if things go wrong on a put, the worst that can happen is you get exercised and are forced to buy 100 shares of the underlying security. You can then turn around and sell covered calls on those shares. You can even roll the put out a couple of weeks or even sixty days if your overall thesis on that position hasn’t changed, probably collecting a bit more premium on the way. Focus on generating cash flow this way as opposed to selling spreads.

Put credit spreads and call credit spreads have indeed created many-a bag-holder on WallStreetBets. That’s why you should only use spreads sparingly. For example, if you have five covered calls and five puts, maybe you can consider one spread, since your premium income is somewhat more diversified. In this scenario, if the spread blows up on you, it’s possible your net cash flow position for the month is still positive.

If you have a small portfolio and the majority of your positions are spreads, a sudden increase in volatility can potentially wipe you out. If this is you, consider taking any profits you can and closing the rest for either a zero-return or possibly even a small loss depending on you potential risk exposure.

Buying shot-in-the-dark growth companies so you can sell covered calls

Covered calls are a safer strategy, and one of my favorites. However, if you have a small portfolio, it may be tempting to buy 100 shares of a cheap stock simply to sell covered calls and generate a $10 or $20 a week. Resist the urge to YOLO your money in this way because you’ll end up with your tail between your legs crying “woe is me” on WallStreetBets. Sure, calls can help you reduce your basis in that lousy stock, but it’s still a lousy stock, and if it goes to zero, you’ll be caught in a vicious cycle of rolling down your strike prices on those calls you sold until you wake up one morning and find yourself disoriented behind the Wendy’s dumpster.

Photo by Trinidad Moreno on Pexels.com Final thoughts

Remember, it’s a lot harder to make money in a bear market. Your goal should be capital preservation. Hold on to your high quality stocks and slowly chip away at your basis in those stocks by selling medium-risk options (.35 deltas) two weeks to 45 days out. Leave some powder dry so you’re ready to sell puts or buy up stocks when you see things bottoming out.

You don’t have to be an economist to try to time the market, because the truth is, no one knows when stocks will rise or fall. Warren Buffet famously says that he doesn’t try to time the market, but common sense will tell you when a good time to buy might be and when you would be better advised to allocate some of your precious capital to the ol’ sock drawer.

Option trading isn’t some scammy “get rich quick” scheme. It requires the investor to build discipline into their trading strategy. Do that, and you’ll be able to generate impressive returns and compound them over the years. In the meantime, if you’re new and you’ve lost some money, don’t let it get you down. Consider any early losses as tuition to learn what not to do. Sometimes, the best way to learn is by making mistakes – just make sure your mistakes are small and infrequent!

-

Why trade options?

Photo by Andrew Neel on Pexels.com Notwithstanding the historic bull run we’ve seen, it’s safe to say that current market conditions demand a bit more attention than simply buying stocks and forgetting they exist. We can all agree that it is somewhat demoralizing buying stocks only to watch them sink or do nothing but collect dust and tie up your capital.

I think anyone who is serious about investing should learn to trade options. Options have gotten a bad rap over the years, but the fact is they are merely derivative products based on the value of underlying securities like Apple or Microsoft.

Options have historically been viewed with suspicion, especially by older investors who have had limited access to them and therefore don’t always understand how they work. As the saying goes: “People fear what they don’t understand.”

“Options are complicated” is a common refrain, but as with most things in life, once you learn the basics, they’re not as scary as they seem. Options offer flexibility, and without their use, there’s simply no way to make money in the stock market other than buying a stock at what you think is a low price at the time and hoping it goes up. This approach to investing is analogous to being a helpless bystander and is not how most successful traders build their portfolios.

Options can be as safe or risky as the strategies you employ. You can make a lot of money really fast, but you can also lose a lot of money really fast. The safest strategy, and what we strive for, is preserving capital while compounding option income over a reasonable time frame. OptionsFlair’s general methodology is to stick with safer strategies while being “net sellers” of options. That is to say we favor selling puts (somewhat bullish) or covered calls (somewhat bearish).

Example of a low-risk option strategy – selling a put

Let’s say you want to purchase 100 shares of Intel (INTC), but it’s currently trading at $35.68 and the most you’re willing to pay is $34. Rather than waiting for it to go down and collecting no money, you can sell a put option one month out for about at a strike price of $34 and collect about $70 of premium up-front. If Intel does not drop, you can repeat this the next month. The annualized ROI for this strategy is about 25%. ($70 option premium times twelve months over the put collateral of $3,400.) Your worst case scenario is the stock drops below the strike price and you are forced to buy the the 100 shares at $34.

An even simpler strategy – selling covered calls

Continuing with the above example, let’s say the price of Intel drops to $33 and you are assigned the shares. As the owner of 100 shares, you are now able to sell covered calls. A covered call is when you sell a call option against 100 shares of a stock you own. Let’s say you are comfortable selling your shares for $36, so you decide to sell a covered call with an expiry date one month away for a premium of $40. Your annualized return on investment is 14%. ($40 option premium times twelve months over the stock purchase price of $3,400.) However, because you also now own the 100 shares of Intel, you are entitled to their dividend, which is about 4% annually. Assuming all your calls expire out-of-the-money, your annualized return is about 18%.

As you can see, simple option trades like this are not as complicated as you’ve been lead to believe. If you’re not using these basic strategies to generate cash from your portfolio, you’re leaving money on the table. The compounding effects of these returns are powerful if you consider that a paltry 6% annual return will double your money in 12 years.

For stocks that are more volatile, your potential annualized returns can be as high as 50% or 60%, but we recommend working with less risky stocks which you are comfortable owning if you are a beginner. After all, an 18% ROI isn’t too shabby, is it?